The Current View

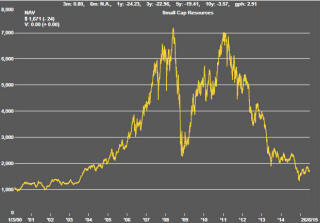

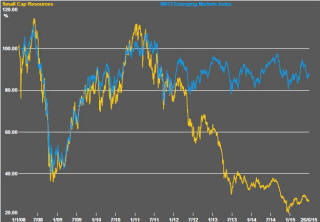

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s illustrated in Chart 4 is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Greece and China gathered momentum as market influences as the week progressed.

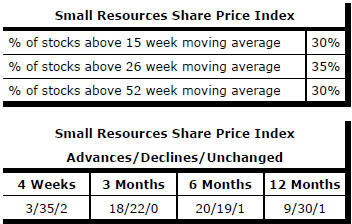

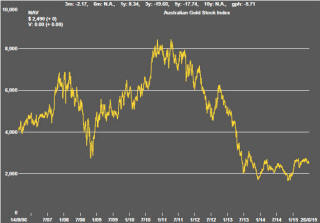

On the resources front, there was nothing in the metal price action suggesting any improvement in cyclical positioning to help move resource sector markets forward. The S&P/ASX 100 resources index lost 3.9% in the week. The small resources share price index fell 3.0%. Further ASX losses could follow the drop in mining equity prices on Friday in Europe.

Within the small resources index, declining stocks heavily outweighed rising stocks with the majority of stocks now trading below their shorter and longer term moving averages.

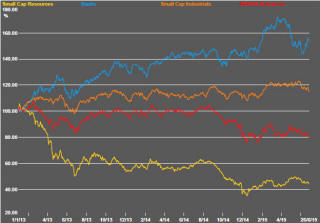

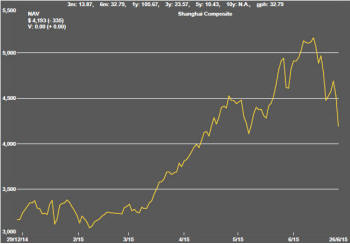

The Shanghai composite index (shown in the chart below)

continued to track lower. It fell 6.4% in the week and is now 18.8% below

its highest recent close. While the Chinese market performance has been a

product of liquidity and regulatory changes, a slump in prices could feed

back into still weaker growth. At least, that is the fear despite a

relatively small proportion of the population being directly involved.

A further cut in Chinese lending rates and reduced reserve requirements announced over the weekend were designed to reassure investors of official backing. Whether in China or elsewhere, such efforts run the risk of simply reinforcing perceptions of an economy in trouble. In China’s case, they might also highlight the diminishing grip on the economy of a once dominant government apparatus.

Observers had been expecting some form of stop-gap agreement between Greece and its creditors over the weekend. That did not happen. All the key political leaders continue to talk about wanting to talk but no one is budging from previously declared positions.

Markets are likely to be destabilised in coming days by the introduction of capital controls and other emergency measures to protect the European banking system. The major European political leaders have expressed confidence in Europe’s capacity to cope with a Greek debt default but there is a nagging doubt that an unanticipated connection to a mainstream financial institution could be uncovered in the event of a default leading to a broader financial crisis.

The Greek government now plans a referendum on whether to accept the European government budgetary reform proposals. With the Greek population seemingly wedded to staying within the European union, the government is at risk of a vote in favour of the austerity measures resulting in another election and the delays in decision making that will bring.

Market Breadth Statistics