The Current View

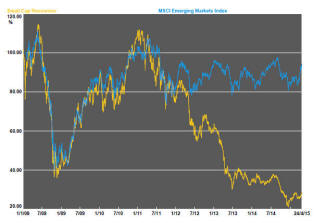

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

A loss of US economic momentum has been a worrying sign for markets generally but a near term rebound in oil prices helped change sentiment somewhat. Also prompted by earnings results which have been slightly better than expected and, within the technology sector, some revenue and earnings gains well ahead of market expectations, equity prices in the USA touched new record levels on Friday.

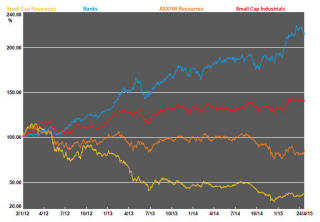

A change in the trajectory of iron ore prices also helped create the scene for a modest rebound in resource sector values. The S&P/ASX 100 resources index rose 4.7% and the small resources share price index added 4.4% during the week.

Companies with iron ore exposure were especially strong. BHP Billiton rose 6.9%, Rio Tinto added 4.9% and Fortescue Metals Group gained 18.2%. Overseas, the share price of the other iron ore market leader, Vale, increased 34.9% over the week.

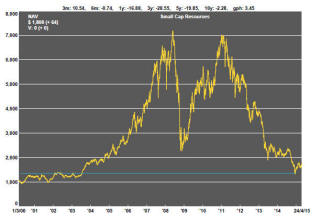

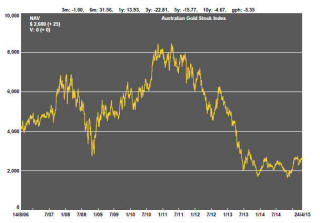

Uranium is another industry segment which has shown

unusual strength. The Global X uranium exchange traded fund rose 11.6%

during the week although, from the longer term perspective displayed in the

chart, last week’s gain hardly makes an impact on the loss of value through

the cycle.

The PortfolioDirect cyclical guidepost suggests little overall improvement in positioning. At best, one could infer that the decline in prices might have stopped.

The prices that have risen most noticeably in the past week have been in industry segments which had previously shown the most intense weakness suggesting that the stronger prices could still prove more of a respite than a change in direction.

At the same time, the price action among the equities in response to these commodity market changes has once again emphasised the extent of the leverage these companies have to signs of cyclical recovery.

Prices have declined to such an extent that unusually strong near term returns may arise without strong evidence of an overall cyclical improvement

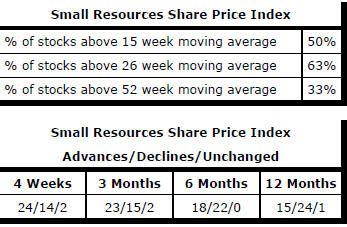

Market Breadth Statistics