The Current View

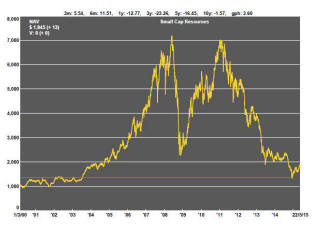

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Equity prices continued to hover around near record levels as volatility dropped. The S&P 500 edged 0.2% higher over the week. The German market rose 3.2%, the FTSE100 added 1.0% and the Shanghai Composite increased a staggering 8.1%.

Once more, markets seemed under the influence of expected changes in monetary conditions. The best place to invest if you expect the Chinese economy to falter, it seems, is China itself. The likelihood that Chinese authorities will allow a sufficient flow of liquidity to maintain the upward trajectory of the market seems enough to keep it moving higher.

The US dollar rose against the euro for the first time in five weeks as expectations of higher US interest rates contributed to further rises.

Federal Reserve chair Janet Yellen gave every sign in a speech on Friday that the Fed is intent on raising interest rates by September. She was prepared to discount the recent growth deceleration as transitory despite it extending well into the second quarter. She expressed a strong belief that inflation would rise and described the labour market as experiencing full employment. The Fed appears to be determined to provide as much forewarning as it is able of an imminent rate rise.

With US rates set to increase, upward pressures on the US dollar are likely to persist. These are conditions in which US dollar denominated commodity prices have always struggled to rise.

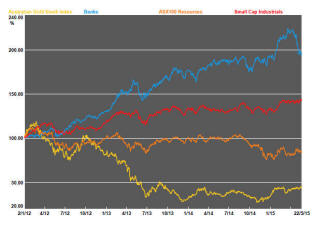

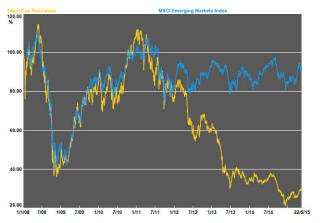

Resources v Banks

Against the run of recent history, resources have outperformed banks during

2015. Since the end of 2014, the ASX small resources share price index has

risen by 19.9% while the banks making up the ASX 200 have lost a net 1.5%.

Before rushing to a judgment about whether this represents a change in market direction, a historical perspective is worthwhile. The chart shows the relative performance between the two market segments since 1992. Viewed this way, the 2015 performance differential in favour of the resource stocks is barely noticeable. It still needs to run some way before a conclusion about a change in market direction can be drawn.

If the 2000-03 experience is any guide, one might be able to (optimistically) infer that the nadir in the resource sector's unfavourable relative performance is getting closer or may be around current prices. Still, the same comparison would imply that several years may have to pass before there is enough momentum created within the resources sector for a meaningful performance differential in favour of resources stocks to become evident.

.

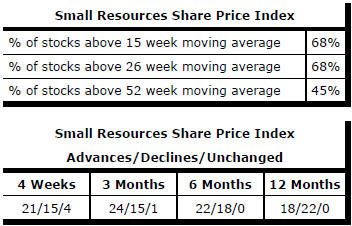

Market Breadth Statistics