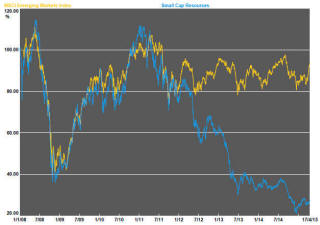

The Current View

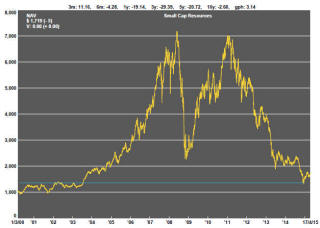

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Equity markets fell sharply at the end of the week through a combination of factors arising in Asia, Europe and the USA.

Against a background of a 30% rise in the Shanghai composite index since the end of February, Chinese market regulators have warned small investors about trading risks and, after markets had closed on Friday, introduced a range of measures which were interpreted as trying to cool market conditions. Constraints were placed on some margin trading arrangements and rules were changed to allow fund managers to lend securities in a bid to increase stock liquidity.

In Europe, the renewed threat of a debt default by the Greek government pushed markets lower. The German market fell 4.4% over the last two trading days of the week. In apparent response to what was happening in Europe and China, the S&P 500 dropped 1.1% on Friday.

Oil prices continued to recover from just over $42/bbl (WTI) in mid March. They have gained 31% since then. The higher prices will have come too late to affect the earnings of energy producers in the first quarter. Lower oil prices, a stronger dollar and weaker domestic demand conditions have resulted in a sharp slowing in earnings growth among those US companies which have reported for the first quarter so far. The slowdown has caused the US market to lose some momentum which had already been dented by the prospect of an impending rise in interest rates by the US Federal Reserve.

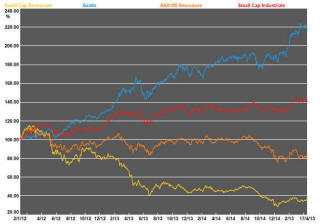

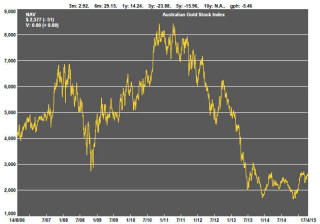

Australia’s small resources share price index rose 5.4% for the week in a gain driven by higher prices for energy stocks. All of the seven best performing stocks in the index, with gains ranging between 11% and 60%, were from the energy sector. Putting these aside, the median change among the remaining stocks in the index was zero. Similarly, the S&P/ASX 100 resources price index was little changed with an increase of 0.2%. The All Ordinaries gold index increased by 0.5%.

On Sunday, the Chinese central bank reduced commercial bank reserve requirements in a bid to spur bank lending and avert further reductions in growth. By showing a willingness to act, the move should prevent fears of a widening market rout in the near term, provided some effect from the measures is perceived. At the same time, the move leaves Chinese equity markets at risk of an unstable equity market bubble as falling property prices and a narrow equity base limit the number of alternative investment options available to Chinese investors.

The

underlying improvement in US labor market conditions - shown here in red as

initial jobless claims on the inverted right hand axis - continues to

highlight one of the reasons for the ongoing strength of US equity markets.

In past cycles, labour market strength has sustained higher equity prices as

it has foreshadowed better business sales conditions while also signalling

greater confidence among business people about their prospects. The

improvement in labour demand has eventually come to an end but, barring an

entirely unanticipated shock, causes of a dramatic reversal in labour market

conditions are not currently evident.

The

underlying improvement in US labor market conditions - shown here in red as

initial jobless claims on the inverted right hand axis - continues to

highlight one of the reasons for the ongoing strength of US equity markets.

In past cycles, labour market strength has sustained higher equity prices as

it has foreshadowed better business sales conditions while also signalling

greater confidence among business people about their prospects. The

improvement in labour demand has eventually come to an end but, barring an

entirely unanticipated shock, causes of a dramatic reversal in labour market

conditions are not currently evident.

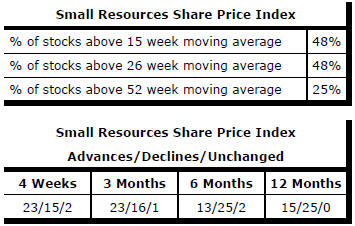

Market Breadth Statistics