The Current View

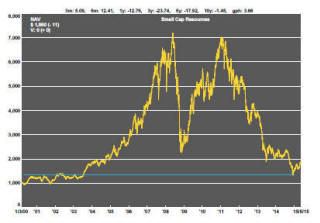

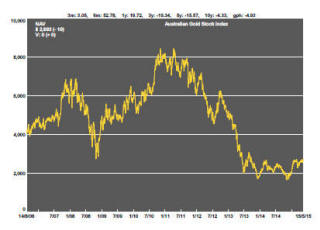

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Markets variously appeared strong and vulnerable in the past week. The S&P 500 passed another record but the most recent moves have been hesitant and, over the week, the gain in the index was only 0.3%.

Bond yields which had been a drag on equity markets were tending lower by the end of the week but US and European yields have been rising and the reversal remains very modest.

Perversely, the threat of weakening economic activity seemed to boost US markets at the end of the week. US economic statistics including first quarter GDP, retail spending, business investment and industrial output are all pointing to a slowing US economy. Slowing growth is creating the impression that interest rate rises will happen less quickly than had been assumed.

Equity markets remain hooked on the flow of funds from central banks as do asset markets more generally. Christie’s, the New York auction house, reported sales of over $1 billion over three days last week including $178 million for a single painting by Picasso.

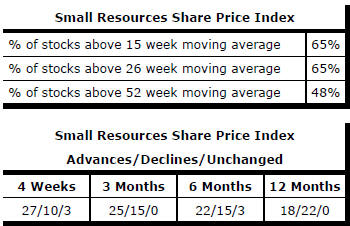

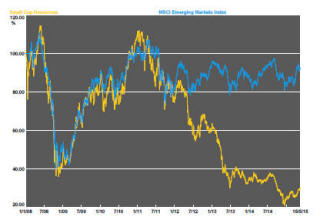

The markets most susceptible to asset price inflation are those depending most on easy money policies now operating in the USA, Europe, Japan and China. Resource sector prices, more heavily dependent on improvements in the real economy, remain anchored to the lower end of their cyclical range. The small resources share price index rose 1.9% during the week and the S&P/ASX 100 resources index increased 2.4%.

Gold Producers Face Divergent Cost

Outcomes

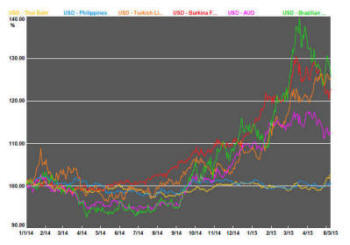

A gold producer in Brazil should be preferred as an investment to one in

Thailand or the Philippines.

Currency markets have become more than

usually volatile over the past six months as the net effect of differing

monetary policy settings across countries have impacted on foreign exchange

markets.

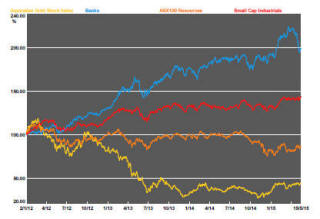

Gold production is an industry with an unusually high and diverse exposure to currency movements. Not all gold producers will have been affected to the same extent by the recent currency moves since they all sell a US dollar denominated product but manage a local currency cost base.

Producers with Australian dollar costs have benefited from an 18% currency depreciation since August 2014 but the gain for companies exposed to costs in Brazil, Turkey and Burkina Faso has been as much as 45%.

As the chart shows, producers in Thailand and the Philippines would be lagging the pack as exchange rate beneficiaries. Some investors might be in for a shock (or a pleasant surprise) if they have been oblivious to the effect on profitability of the relative currency movements.

Gold and Silver Tussle for

Ascendency

The gold price has stretched its link to silver to the upper end of a

relatively well-defined historical range.

There

is no law of nature that says gold prices cannot go higher without silver

following. Even so, the two markets have so many traders tracking these

arcane relationships that they seem to stand a good chance of remaining

intact.

There

is no law of nature that says gold prices cannot go higher without silver

following. Even so, the two markets have so many traders tracking these

arcane relationships that they seem to stand a good chance of remaining

intact.

It is hard to imagine silver prices rising firmly in the event gold prices fall convincingly, leaving any resolution of the trading pattern to depend on silver prices falling by less than a fall in gold prices or by displaying unusual leverage to a rise in the gold price.

Market Breadth Statistics