The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

The large directional moves which had typified equity, bond and currency markets for several months here to have faltered if not come to an end.

Greek debt negotiations and guesses about future Federal Reserve policy have added to market volatility without providing a sense of direction for markets. By the end of the week, the International Monetary Fund had left the negotiations with their Greek counterparts expressing pessimism over whether a solution could be found to the impasse between what the IMF and European governments were seeking, on the one hand, and what the Greek government was prepared to concede, on the other.

Markets are bracing for the repercussions of a default while implicitly assuming that the consequences will be confined to those parties most immediately involved.

Obstacles to a Federal Reserve rate increase appeared to have been removed with recently released statistics pointing to some strengthening in U.S. consumer sentiment. Fed-watchers are generally of the view that the first rise is more likely in September than in June but the Fed chair is scheduled to speak to the press after the policy committee meeting this week giving the meeting, whatever its decision, added importance as a source of market instability.

The OPEC meeting in Vienna took no overt action to cut production. None was expected but there are reports of Saudi Arabian negotiations to supply crude oil to India which would add to global output.

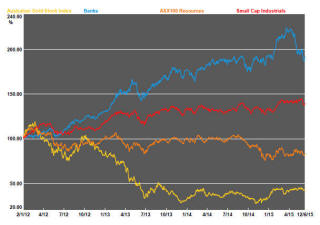

Falling resource sector share price volatility has been helping support a gentle rise in prices. The small resources share price index rose another 1.5% last week. A similar rise of 1.2% was made by the S&P/ASX 100 resources index. Bank shares also rose 1.5% although prices finished the week 5.0% lower than they had been at the end of May.

U.S. bond yields ended the week slightly lower after earlier reaching the highest levels since September 2014. U.S. equity prices remained in a similarly narrow range with the S&P 500 finishing with little change over the week. The U.S. dollar also edged lower in the latter part of the week to end 1.4% below where it had been a week earlier.

While these price variations suggested some reduction in volatility and the possibility of some change in direction after lengthy seemingly one way moves in bond, currency and equity markets, the ongoing failure to agree a Greek debt solution and uncertainty about the timing of an interest rate rise in the USA will keep open the possibility of a resumption in a similarly large directional moves in the balance of 2015. .

Market Breadth Statistics