The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Government bond yields, the US dollar exchange rate, emerging market stock prices and the prices of some commodities, such as oil, changed direction during the week. European and US equity markets finished the week pushing higher supported by the reversal in bond yields.

The major economies have evolved in recent months to the point where, in Europe, the USA, Japan and China, there is increasing conjecture about the likely near term trajectory. As a consequence, markets are responding increasingly to individual pieces of information without necessarily producing a firm sense of direction.

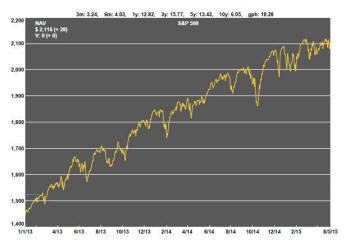

The S&P 500 is one indicator of this lost momentum. In

the absence of a fresh reason to go higher or a conclusive source of

weakness, it finished close to being unchanged during the week despite

traversing a 40 point range. While it did so, it stayed within the same

trading band it has occupied since early February.

The market rise on Friday from the bottom of the trading range came after the release of monthly labour force statistics. The employment growth in April was strong enough to encourage a belief that the economy was continuing to expand at a pace consistent with moderate earnings growth without being so strong as to raise the prospect of an aggressive change in Federal Reserve monetary policy.

The surprisingly strong electoral showing by the British Conservative Party in UK national elections helped buoy UK equity markets and sterling. The palpable sense of relief displayed in the immediate aftermath of the election result might yet give way to worries about the policy outlook. Ahead are another round of negotiations with advocates of Scottish independence and a deal aimed at deciding whether the UK will quit the European Union.

After the Reserve Bank of Australia decided to cut its policy rate by another 0.25 percentage points, the Australian dollar rose and has remained at elevated levels despite attempts by the central bank to push it lower. Expectations of a fall in the currency are likely to deter foreign investors, at the margin, from entering Australian dollar markets. A prolonged period of currency resilience may eventually attract more overseas interest. Until then, the local equity market is at risk of further weakness.

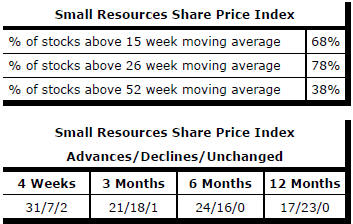

The S&P/ASX 200 share price index fell 3.1% during the week driven by a 5.6% fall in the price of bank shares. The S&P/ASX 100 resources index fell similarly, by 3.2%. The small resources share price index fell a more modest 0.4% with a further improvement in the breadth of the market. Three quarters of the stocks comprising the index showed positive returns over the past four weeks.

Market Breadth Statistics