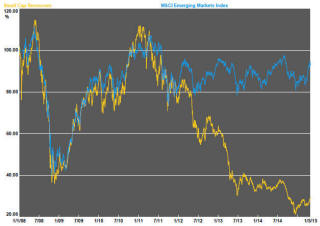

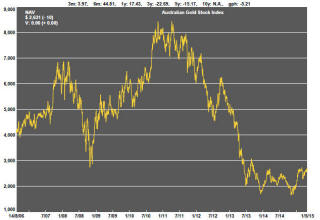

The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable. That remains a possible scenario for sector prices.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

The lower equity prices fall - and the higher the cost of capital faced by development companies - the harder it becomes to justify project investments. The market is now entering a period prone to even greater disappointment about project delivery .

Has Anything Changed?

The assumption that June 2013 had been the cyclical trough for the market now appears premature.

Sector prices have adjusted to the next level of support. The parallel with the 1990s is being tested. Prices will have to stabilise around current levels for several months for the thesis to hold.

Key Outcomes in the Past Week

Mixed messages permeated financial markets through the week resulting in some large daily equity and bond price movements without a clear direction being evident. The S&P500 rose and fell on successive days to end with no material change through the week.

Government bond yields rose again. US 10 year yields finished at 2.11% on Friday having been at 1.87% two weeks earlier. Over the same period, German yields have risen 29 basis points.

The threat of a Greek default came and went with a broadening consensus that the Greek government will reach an agreement with European finance ministers especially since the Greek finance minister, who was widely criticised for being too aggressive, had been sidelined as the principal negotiator on the Greek side. Greek 10 year bond yields declined 7.25 percentage points during the week.

The Australian stock market was generally weaker with banking stocks falling 3.7% after rising fears of a slowdown in activity and uncertainty about whether the Reserve Bank will cut interest rates at its next meeting. The broader Australian market fell 1.6%. Within the resources sector, the small resources share price index rose 1.9%. The S&P/ASX 100 resources index was 1.0% higher.

The US dollar which had been on an upward trajectory since June 2014 lost some momentum. The evidence of weakening economic data would have played a role. At the same time, the weaker currency would have helped allay some concerns about flagging corporate earnings.

Weaker US economic data ended up causing minimal discomfort after a 1.0% S&P500 fall on Thursday hinted at something more severe to come. Weather related transitory effects appear to have been readily accepted as an excuse with a recent history of compensating growth after other weather-induced lulls in activity coloured interpretations.

The weaker US dollar had a beneficial effect on metal prices. The PortfolioDirect cyclical indicator has shown the largest upward movement in over a year. inferences about the pace of global growth from iron ore and oil prices are pressing less heavily on the metal markets now that the prices of those two commodities have steadied and improved somewhat.

Iron ore prices rose after BHP Billiton flagged that it was not going to proceed with a Pilbara port expansion which would have added around 20Mtpa to exports. At the end of the week, Vale had also raised doubts about whether it would proceed with the full slate of expansions it had foreshadowed. Mid-week, the CEO of Cliffs Natural Resources attacked the iron ore majors for “terrorising” the market by threatening unnecessary increases in supply and asserted his view that the threats to expand production would not eventuate.

A flow of news about energy storage technology excited some additional investor interest in lithium. The Global X lithium exchange traded fund rose 3.9% during the week and 7.5% over two weeks. There have been other isolated signs of improving interested in the sector on global markets. The Freeport McMoran share price has risen 27.2% over the past three weeks and is threatening to move past levels which had previously constrained performance.

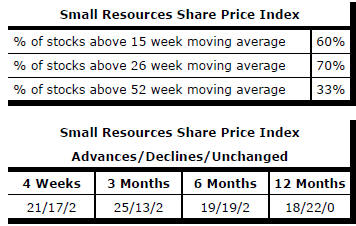

Market Breadth Statistics