The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

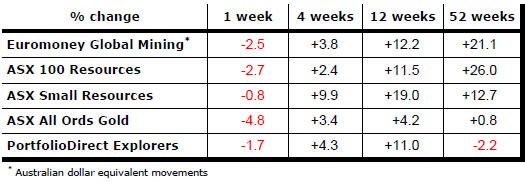

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

Market Breadth Statistics

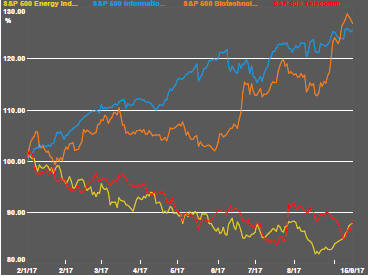

Across the board sectoral price gains pushed U.S. markets to new record levels (see right hand panel).

The previously weakest sectors - telecommunications and energy - made gains. The energy sector has more or less fully recovered from its most recent historical lows to prices which had prevailed earlier in 2017, breaking the evident downtrend in prices.

The U.S. dollar remained near multi-year lows. Ample scope remains for the currency to move lower with a near term test possibly coming shortly from the Federal Reserve after it decides in the coming week to disclose the timing of its next steps to unwind holdings of securities accumulated since 2008.

U.S. bond yields have turned up - possibly in anticipation of reduced Federal Reserve influence on security pricing in financial markets.

The reversal in the direction of U.S. yields in the past week coincided with a weakening of copper prices despite the metal price more often moving in concert with bond yields reflecting trends in economic activity and inflation to which they are both sensitive .

The link between bond yields and copper prices has appeared broken for several weeks as the effect of U.S. dollar weakening on copper prices has overshadowed the connection to the real economy.

A rising yield, as the Federal Reserve begins unwinding its balance sheet combined with a firmer U.S. dollar due to policy tightening, potentially puts of the copper price at risk in the absence of a change in real output growth in the major economies.

Beyond copper, the broader range of daily traded non-ferrous metal prices also weakened through the week although the tin price has remained the odd one out once again.

Gold prices were also tangled up with movements in financial markets. The leverage to exchange rate movements and bond prices combined to produce a modest decline in gold prices as they fell short of the most recent high levels.

Gold-related equity prices had been propelled higher by the most recent gold bullion price trend breaking the loss in momentum among gold equity prices which had been apparent throughout the past year. The turn in equity prices was consistent with the bullion move in the past week.

The smaller end of the golden equity market has underperformed the bullion price movement.

Palladium prices have been trending higher since the beginning of 2016. They are now trading at levels which suggest a risk of significant downside even within the context of a longer term rising trend being maintained.

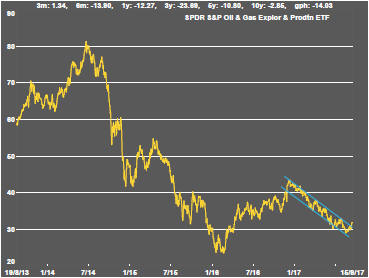

Oil and gas exploration stocks, consistent with the broader energy sector, had moved to the upper end of their downtrend with suggestions now of having begun a directional shift.

The uranium sector, along with tin related stocks, are now the two segments of the mining market which have appeared untouched by the recently more buoyant market conditions.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.