The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

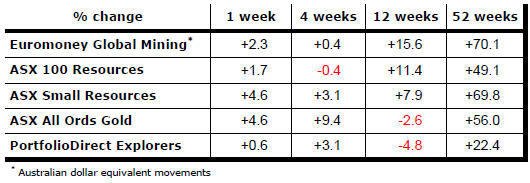

Key Outcomes in the Past Week

Market Breadth Statistics

The key investment question at the start of 2017 is whether too much improvement in underlying economic conditions has already been factored into rising equity prices.

The track of the small resources share price index shown in the first chart opposite provides a partial answer to this question in respect of the resources sector.

Despite seemingly dramatic sector equity price improvements since late 2015, most noticeably in the first half of 2016, prices now differ little from those which had been regarded as unsatisfactory and historically weak in the third quarter of 2014. This is consistent with persistence of a late 1990s type of sector price environement.

Copper and iron ore prices which had driven much of the renewed appeal of the leading stocks in the sector have lost momentum.

While evidence of an improvement in Chinese manufacturing conditions would have contributed to the rise in prices of these two principal industrial commodities, the loss of upward price momentum also coincides with a loss of momentum in the growth prospects of the Chines economy.

Some improvement in copper and iron ore prices will have been warranted, especially given the sensitivity of the commodity markets to changes in the momentum of growth near the bottom of a cycle. Without further support, the balance will begin to tilt in the other direction.

A pattern of relatively minor momentum shifts is emerging. These could persist in the absence of a systemic scare of the type which has disrupted markets in recent years.

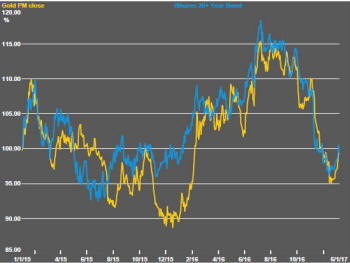

Gold prices have contributed to positive sector performance in the past week but have continued to track bond prices. With a strong likelihood of lower US bond prices over the coming year as US interest rates head toward more sustainable levels less dependent on Federal reserve market intervention, downside risks for gold prices persist.

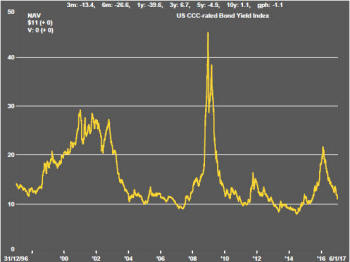

Contrary to the direction of government bond yields, lower grade corporate bond yields have continued to decline. This suggests greater confidence among investors about the risk profile of the resources sector, particularly oil and gas companies, and generally more favourable funding conditions for companies seeking to fund higher risk development projects.

While a wide range of commodity segments have shown significant improvement, uranium has been trading near cyclically low prices, at least when measured by spot prices. While the move has yet to prove conclusive, the momentum of uranium related equity prices appears to be improving.

Working against the potentially improved funding environment for resource sector equities has been the strongest U.S. dollar in 14 years. The currency strength threatens to cap the rise in commodity prices and, in the absence of better global growth outcomes, possibly force prices lower.

Companies borrowing US dollars will have to take care in managing repayment obligations with the balance of risks continuing to favour rises in the currency for possibly a year or more even in the event tat it is destined to revert to the longer term downtrend depicted in the second of the cyclical guidepost charts on page 1.

.

The Steak or Sizzle? blog LINK contains additional commentary on the sources of the share price performance among the best performed stocks and the extent to which these near term investment outcomes might be underpinned by a strong enough value proposition to sustain the price outcomes.