The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

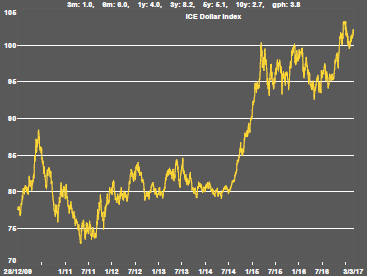

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Key Outcomes in the Past Week

Market Breadth Statistics

The highlight of the week for markets was the speech by Federal Reserve chair Janet Yellen to a business gathering in Chicago on Friday.

Yellen came as close as a Fed chair does to foreshadowing a policy change as she referred to her expectation that FOMC policymakers will raise the target Fed Funds rate when they meet in the middle of March.

Yellen also appeared to endorse the idea of three rate rises during 2017 as the Fed pushes ahead to normalise policy settings as its inflation and employment goals are achieved.

The Fed chair also said, in the course of her remarks, that she saw the risks to the global economy as being more balanced, giving policymakers more confidence that their decisions would not be derailed by external events.

Bond yields changed little after the Yellen speech as financial markets appeared to take the latest move in their stride.

At least for the time being, markets appear to accept that they have adequately anticipated higher inflation and the policy approach being implemented.

In some respects, the Fed has had some pressure removed with the installation of the Trump administration which is aiming to play a larger role in setting the economic agenda than was the case under President Obama.

The trajectory of US interest rates is consistent with further upward pressure on the US dollar.

A higher dollar could start to crimp growth and inflation. Whatever the ultimate level to which the dollar ascends, the Fed is likely to be less influenced in its decisions if the pace of rise is moderate enough for business to become gradually conditioned to the changing environment than if the currency undergoes a large change over a short time period.

The US dollar movements were putting pressure on commodity prices. Together with unfavourable movements in US inventories, oil prices fell and sector equity prices, which had previously showed signs of stalling, moved lower as a consequence.

Gold prices, which had moved more aggressively than other financial prices, lost momentum raising the possibility of a fall to levels around US$1140/oz.

Copper and iron ore prices have largely retained the gains made in the second half of 2016, helped by how China is delaying its transition to a lower sustainable growth rate.

Having stabilised growth outcomes, there is limited prospect of further upward pressure from China as the leadership meets to set new targets for restructuring of the economy.

The relative stability recently in the more broadly based CRB commodity price index, which includes agricultural and energy prices as well as those for raw materials, suggests some important macro growth constraints on prices impacting all of the principal markets.

The current pace of global growth appears consistent with price stability and a possibly prolonged cyclical trough after the early 2016 return to 2015 prices.

The upturn in uranium related equity prices which had been a recent market highlight has lost some power.

The sector which has fallen short of recapturing losses made since mid 2015 is also constrained by a bottom of the cycle anchoring in price expectations.

Apparently large percentage gains, higher than seen for four or five years, have attracted stronger investor interest but also encouraged holders to take profits.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.