The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

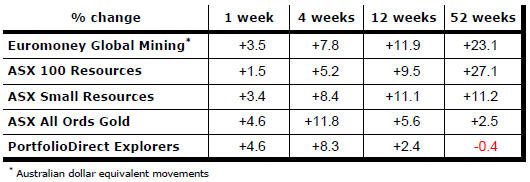

Key Outcomes in the Past Week

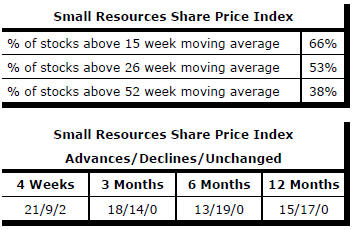

Market Breadth Statistics

Market volatility which had been lifted by U.S. political controversies and the evolving battle of wills with North Korea reverted to near record low levels.

Biotechnology stocks performed impressively in a still bifurcated market.

Financial services stocks have been hindered by doubts about whether previously anticipated favourable regulatory changes will be implemented and by some narrowing in interest rate spreads impeding of the buildup in profitability for lenders.

Emerging market equity prices pushed to levels at the upper end of the range for these markets over the past six years.

The U.S. dollar has continued its downward bias against the currencies of the major trading partners of the USA.

The Chinese currency has maintained its impressive upward trajectory making it harder for other countries to claim currency manipulation is unfairly affecting trade balances.

The change in currency direction also modifies some of the impact on Chinese resident companies from higher commodity prices.

U.S. dollar denominated gold prices have been one of the beneficiaries of a weaker U.S. dollar.

Some commentators would also claim that rising geopolitical risks have contributed to higher precious metal prices. That may be so at the margin but the move in gold prices has largely tracked the pattern of U.S. bond markets which, together with the currency, suggest that the dominant influence on gold prices has been re-pricing of financial market assets.

And

The prices of gold-related equities have been responding more strongly to bullion price movements although the equity price performance through 2017 has been relatively subdued suggesting that adverse equity market conditions have offset the normally expected equity price leverage to higher gold prices.

Australian dollar denominated gold equity prices have been more responsive to bullion price movements.

Within the precious metal grouping, palladium prices have remained in an uptrend dating from the beginning of 2016.

Platinum prices have lagged the group although all the major precious metal prices have moved higher over the past week reflecting a broad based change in financial market sentiment.

Among non-ferrous industrial metals, prices generally moved higher with only tin, of the major daily traded metals, being an outlier in a re-pricing of the sector. Aluminium, copper, zinc and nickel prices traded at their highest levels for 2017. Lead prices were close to peak levels.

The uranium sector has remained within a narrowly defined cyclical trough.

Crude oil prices have been affected by reduced refinery demand due to refinery closures forced by U.S. cyclone Harvey but the related equity prices firmed slightly in anticipation of disruption to crude production in the aftermath of the cyclone.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.