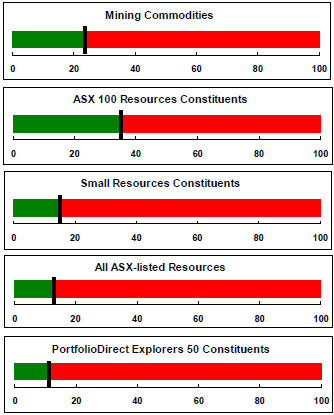

The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

Resource Sector Weekly Returns

Market Breadth Statistics

52 Week Price Ranges

Equity Markets

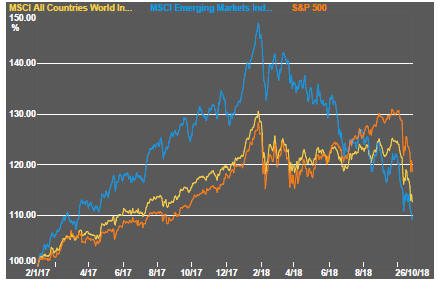

The equity sell-off gathered force during the week punctuated by strong intraday swings in prices. The emerging market index reverted to levels touched in the first quarter of 2017 as other markets gave up the gains which had been made during 2018.

Nervousness about earnings influenced US market conditions. Even where third quarter earnings met expectations, investors were preoccupied with the outlook for the year ahead when earnings growth rates are expected to be substantially lower and the negative effects on profitability of a trade dispute with China more evident.

Technology stocks were especially vulnerable in the sell-off having acquired in their prices a large premium for growth despite evidence of economic growth within the USA and overseas starting to slide. For some of the technology stocks, newly emerging regulatory problems have also become a more readily evident headwind.

Rising short term interest rates which caused a flattening in the yield structure during the week had a detrimental effect on financial sector stock prices.

The outlook for monetary policy settings was another strong influence more generally with growing anxiety over the possibility of the US Federal Reserve taking a more aggressive approach to tightening monetary conditions. Even among those who do not expect the Fed to tighten more than forecast, there is a worry that the pace of economic activity will be damaged.

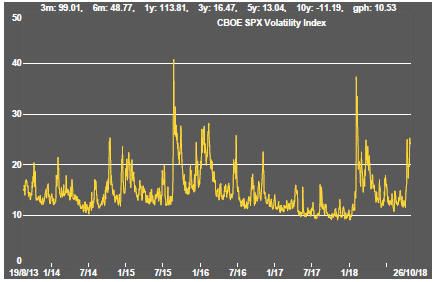

The spike in expected volatility stayed within the bounds of what had happened previously over the past three years suggesting that investors were not panicking unusually. While some of the more expensive market segments conspicuously lost ground, buying in less high profile segments of the market was occurring, consistent with only a modest correction by historical standards.

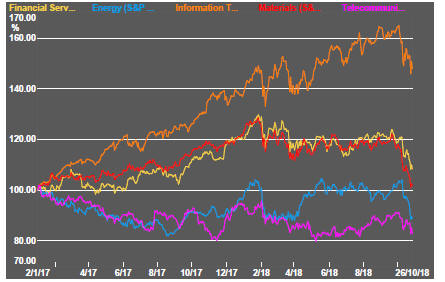

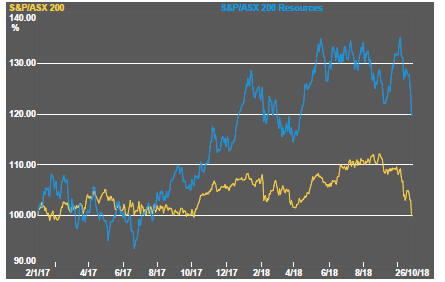

Resource Sector Equities

Resource sector equities were caught up in the sell-off with losses evident across all development phases of the industry.

The performance of Australian listed mining companies, which had been relatively strong, deteriorated sharply although the Australian sector has retained most of the relative performance gains made over the past year.

Gold related stocks posted a modest gain, against the overall sector trend.

While losses were broadly based, the prices of exploration stocks fell by more than the larger stocks in the sector.

Interest Rates

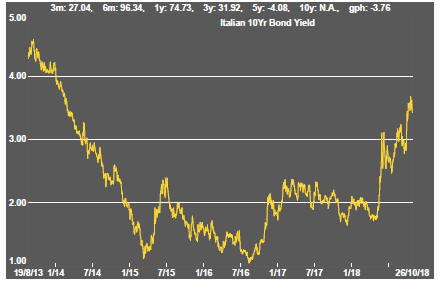

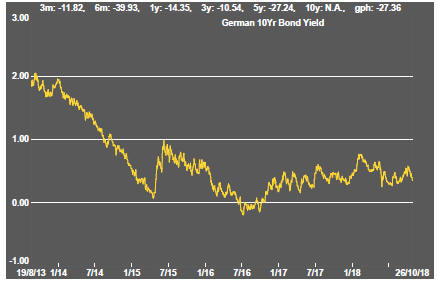

US government bond yields flicked higher but losses have been curtailed by the pursuit of safe havens during the equity sell-off. German government bond prices have benefited similarly with uncertainties over Italian budget policy being an additional factor influencing European capital flows.

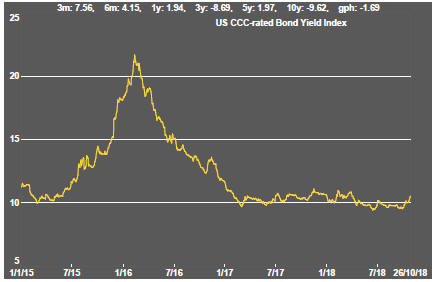

High risk corporate bond yields have not moved dramatically but have begun an upward trajectory in an ominous sign for mining companies looking to fund development activities.

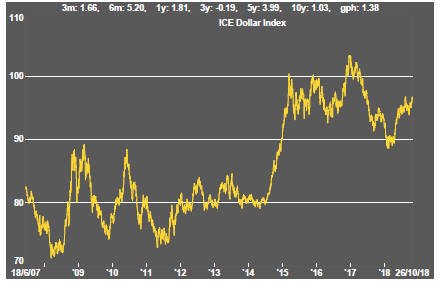

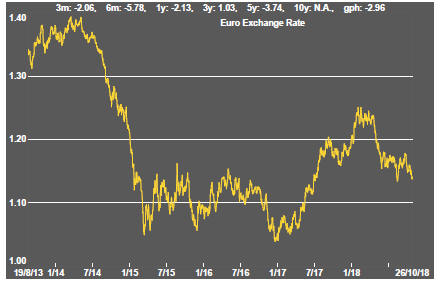

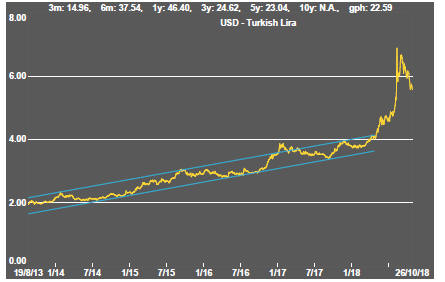

Exchange Rates

The US dollar pushed higher, also reflecting pursuit of lower risk destinations, as both the euro and sterling edged lower. Sterling was hurt later in the week by a Bloomberg report citing a failure among UK cabinet ministers to reach agreement on Brexit terms despite several having claimed that the vast majority of matters needing agreement with Europe have been dealt with satisfactorily.

Statistics relating to European growth also showed a momentum loss with a consequentially beneficial effect on the US dollar. While several important economic indicators have been favouring a stronger dollar, data relating to US investment spending and trade flows are indicating a slowing economy and are ameliorating some of the upward pressures.

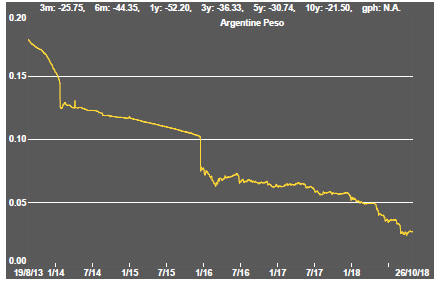

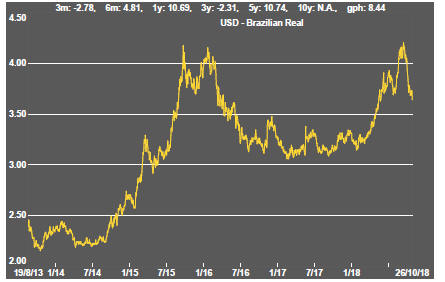

The deterioration in emerging market currencies has become less pronounced although the Indian and Chinese currencies are still caught in conspicuously weakening trends, as is the Australian dollar. The Chinese move relates, in part, to the Sino-US trade dispute. For India, political uncertainty in the run up to state and national elections is a factor. Election results in Brazil, where a conservative has been elected president, have raised expectations of a crackdown on corruption and support for more business oriented policies.

Commodity Prices

The general upswing in commodity prices since mid 2017 had been given added impetus by stronger crude oil prices.

Diminished momentum has left prices within the bounds of a cyclical trough, albeit at the upper end.

The flip side of the benefits for commodity producers and exporters of higher commodity prices is the cost pressure now being experienced by users of agricultural and raw material commodities. Reporting companies have been suggesting this as a source of margin compression.

Business surveys closely watched by central banks are showing signs of upward pressure on selling prices as a result of higher raw material prices.

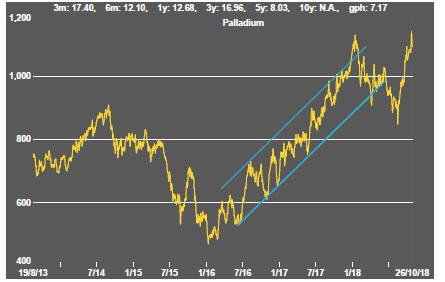

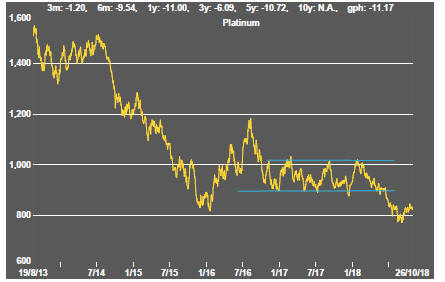

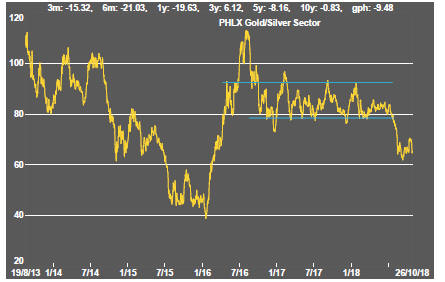

Gold & Precious Metals

The gold price moved up modestly in the context of an accelerating rout in equity prices. Expectations of higher interest rates will have modified some tendency to use gold and other precious metals as safe haven investments.

Within the US markets, gold related equities displayed a stronger correlation with declining equity price indices than in Australia where the correlation between equity and bullion prices has been stronger.

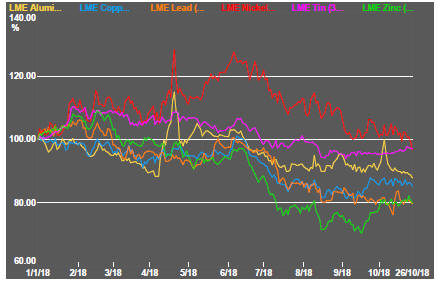

Nonferrous Metals

Daily traded non ferrous metal prices have been tending lower with only tin and lead being able to hold the line in the past week. Overall, the daily traded metal prices are consistent with a cyclical peak having occurred in February 2018.

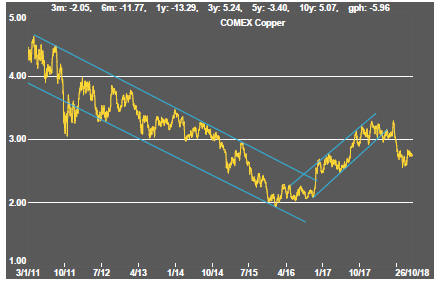

The copper price remains at odds with rising bond yields which normally signal strengthening inflation and growth. The normally growth sensitive metal price appears to be taking a back seat as an indicator of market conditions for the time being.

Bulk Commodities

Chinese economic growth reports show the national economy meeting its targets, as one would expect for a centrally planned economy, but without any overt signs of upside risk. The tariff fight with the USA is beginning to take a toll on activity rates in an economy with a bias toward less strong growth in the years ahead.

The latest manufacturers purchasing managers index for China, measuring conditions in September, implied a slowing momentum albeit within the context of a still expanding sector. The fall in the monthly reading was the largest since October 2017.

Reported GDP growth in the September quarter was consistent with official forecasts although hitting the targets is becoming more challenging by the year.

Iron ore prices continued to gain ground and, among the main mining commodities, are now one of the few sources of metal price strength over the past year.

Coal prices, which had shown signs of losing momentum - albeit after some strong gains - slipped slightly during the week. China reported growth in coal output between September and August and over the year to September with plans to open new capacity proceeding as the country switches to larger more efficient sources of coal production.

Oil and Gas

Crude oil prices dropped again as concerns about demand growth loomed and supply constraints appeared looser.

OPEC has been losing control of the market as US and Russian production has become more significant and while several OPEC members lose their historical clout.

Reimposition of Iranian economic sanctions by the US government has put upward pressure on prices. The failure of effective government in Venezuela has been another contributing influence on higher prices.

The Iranians have been lobbying European countries to prevent more widespread application of sanctions but the likelihood of relief appears slim as long as funds must circulate through US banks.

US production, in any event, continues to rise and is now matching output from Russia and Saudi Arabia. Texas alone is positioned to be the third largest producer after Russia and Saudi Arabia. Export infrastructure limitations may be the greatest impediment to US production having a greater effect on international energy prices.

US stock holdings continue to rise impacting the structure of WTI futures prices.

OPEC also disclosed in its last monthly market report that it expected demand for crude to grow less strongly in 2019 than it had previously forecast in another sign of the decelerating global economy.

The prices of oil related equities have reacted negatively to the weakening market conditions with the added pressures coming from slumping equity prices.

Battery Metals

Eighteen months of rising lithium-related stock prices have given way to a prolonged period of market reassessment as a lengthy pipeline of potential new projects has raised the prospect of ongoing supplies better matching expected needs.

Potential lithium producers have been able to respond far more quickly to market signals than has been the case in other segments of the mining industry where development prospects have been slowed by reticence among financiers to back development.

Movements in lithium related equity prices had been aligned more closely with overall sector equity prices in recent weeks with the lithium stocks tending to display a greater leverage to changes in market sentiment about the mining sector.

The median fall from their 52 week high within a large sample of 80 Australian and Canadian listed stocks with lithium exposure, mostly with an exploration orientation, has been 56%. Every one is trading below its peak price from the last year.

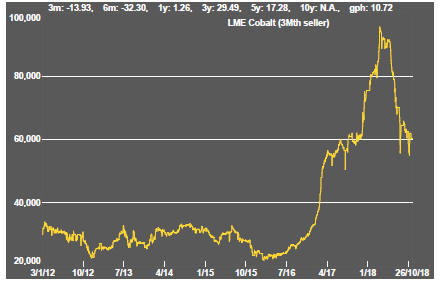

Battery metals remain a focal point for investors with recent attention moving to cobalt and vanadium.

Doubts about political conditions in the Democratic Republic of the Congo (and instances of Ebola) have added a dimension to cobalt prices lacking in other metals caught up in the excitement over the longer term impact of transport electrification.

In the longer term, cobalt is the most vulnerable of the battery related metals to substitution with high prices likely to stimulate research in that direction.

A spokesperson for Panasonic, manufacturer of batteries for Tesla motor vehicles, has been quoted as saying that the company intends to halve the cobalt content of its batteries because of uncertainties over supply although, offsetting such a move, will be the rapid increase in the number of units produced.

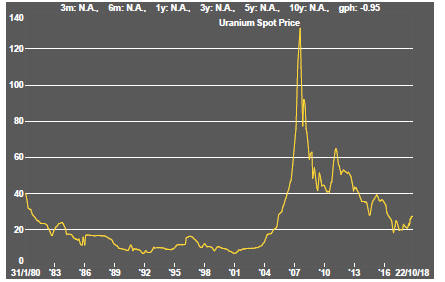

Uranium

The uranium sector is in the midst of forming a prolonged cyclical trough as market balances slowly improve. Power utilities are still reluctant to re-enter the market for contracted amounts of metal to meet longer term needs. An upward bias in prices has been evident in the past month.

Slightly higher equity prices from time to time, in the hope of improved conditions, have not been sustained but could be repeated as speculation about improved future demand ebbs and flows. The effect of an announcement by Canadian producer Cameco to extend the duration of its previously implemented production cut gave the market a very slight but quickly lost lift.

News that the Kazakhstan government intends to list its state owned uranium producer and the world's largest producer, may suggest greater responsiveness to market conditions and less emphasis on production to maximise government revenue.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.