The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

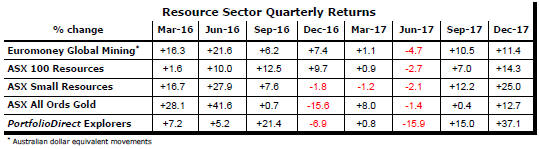

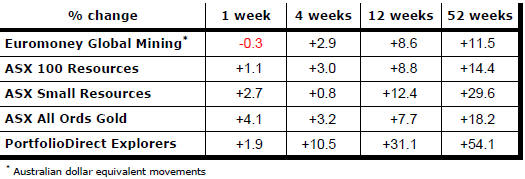

Resource Sector Weekly Returns

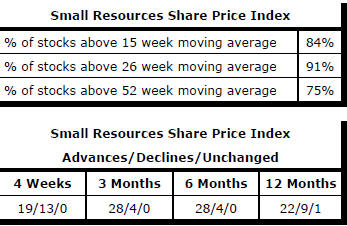

Market Breadth Statistics

International equity markets - in advanced and emerging economies - continued to trade at or near record levels to produce outstanding start of the year returns.

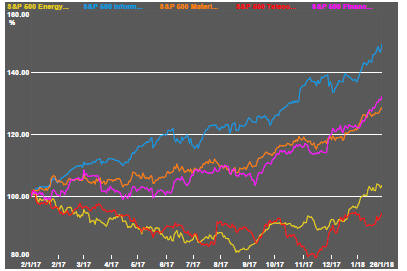

The US market continues to display a marked sectoral disparity in price outcomes.

Considerations of tax policy have dominated US equity prices with earnings estimates being progressively reappraised.

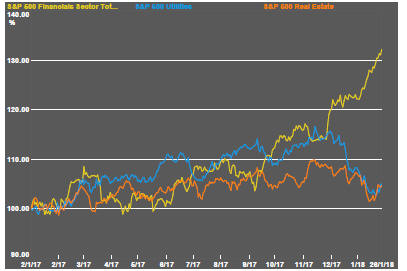

Interest rate impacts are also more evident with a widening gap between the share price performance of financial services companies which are thought to benefit from higher rates and real estate and utility prices which are less favourably impacted.

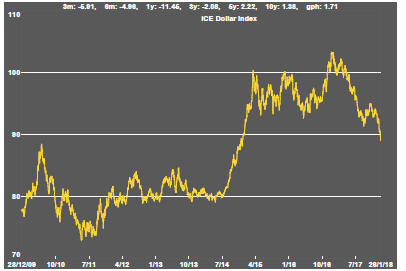

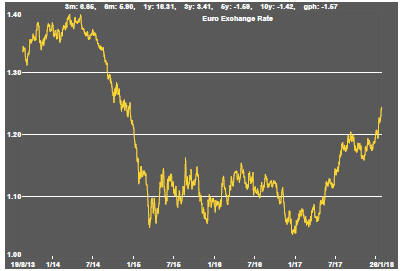

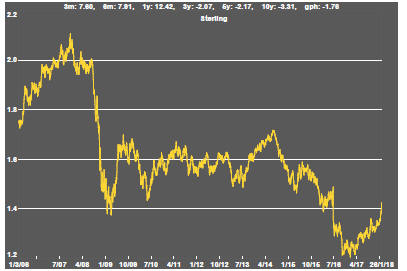

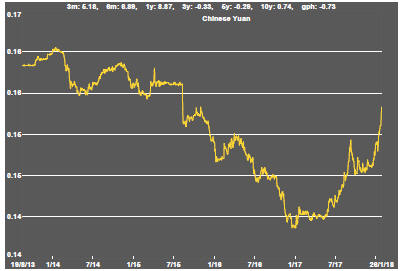

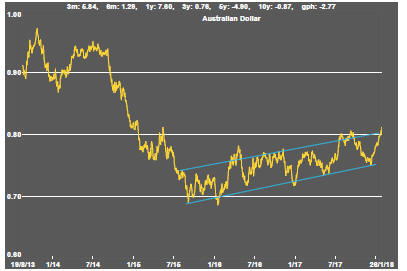

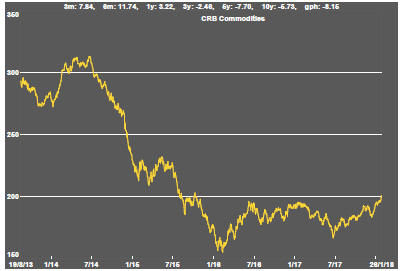

Changes in the direction of currencies have been a recently prominent feature of markets generally with a specific impact on the commodity segment.

Despite a more optimistic tone to commentaries about US economic growth and the prospect of further US interest rate rises, the US dollar has weakened. Such a move is not unusual during relatively buoyant market conditions as the role of the US currency as a safe haven is less sought after and capital flows into more risky envirnements.

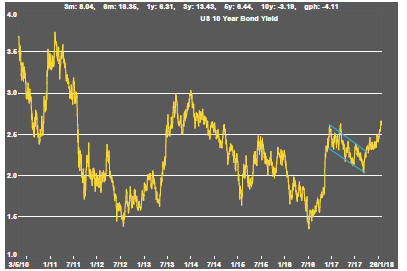

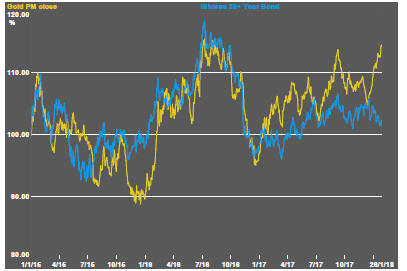

US bond yields have risen as the US growth outlook appears to have strengthened and as confidence gathers that interest rates will move closer toward more normal settings, even possibly faster than had been anticipated previously.

More favourable growth conditions and the weaker US dollar have helped support generally higher commodity prices.

Despite weaker bond prices (which would normally detract from gold prices), gold prices have risen as one would expect with the downtrend in the US dollar.

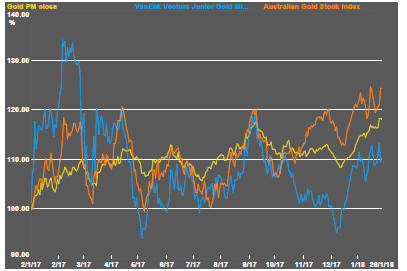

Related equities have proven more volatile but have also tracked higher. Unsurprisingly, given previous strong performance and the appreciating Australian dollar, there has been less leverage to the higher bullion price among Australian listed equites.

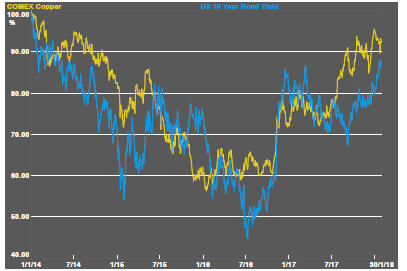

The combination of higher bond yields, which would normally signal rising demand for raw materials, and the weaker US dollar have helped support higher copper prices although the extent of the leverage has been moderate by historical standards.

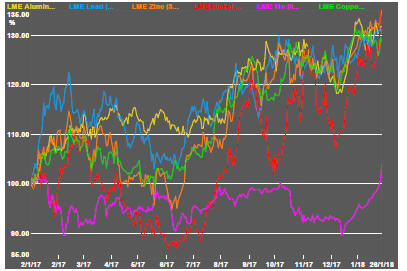

The major daily traded nonferrous metal prices are closing January very near their peak levels from over the past year and all but tin are converging on very similar increases since the beginning of 2017.

Although the tin price has fallen well short of the gains among the other metal prices over the pas year, more recent gains have been as strong as for other metals in the segments.

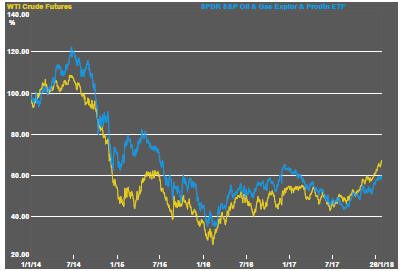

Continued strength in crude oil prices has supported higher equity prices among oil and gas exploration and production companies.

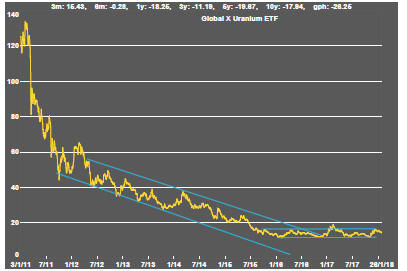

The uranium equity sector has remained within its trough formation having given up the very modest improvement which came after recent announcements by two of the major producers that they would cut production and partially supply customers with material bought on the spot market.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.