The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were largely reversed through the first half of 2016 although sector prices have done little more than revert to mid-2015 levels.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

A 1990s scenario remains the closest historical parallel although the strength of the US dollar exchange rate since mid 2014 has added an unusual weight to US dollar prices.

The first signs of cyclical stabilisation in sector equity prices have started to show. This has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development may have passed its most difficult phase at the end of 2015 with signs of deals being done and evidence that capital is available for suitably structured transactions.

Resource Sector Weekly Returns

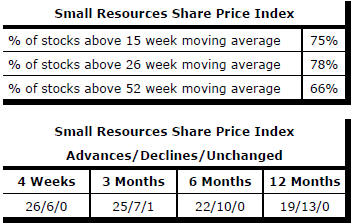

Market Breadth Statistics

Despite near records among major equity price indices, divergent sectoral patterns persist with information technology heading S&P500 outcomes to date in 2017 and telecommunications bringing up the rear with a improving energy sector.

Market volatility indicators remain extraordinarily low signifying a broad absence of concern about high market levels or the loss of power among the principal drivers of equity market performance.

Government bond yields have remained within tight bounds suggesting little concerns about inflation or the likelihood of unexpectedly strong growth which might stoke stronger inflation.

The bond market outcomes remain at odds with the drive for higher short term rates by the Federal Reserve which is preoccupied with normalising rates to create more future flexibility.

The narrowing of interest rate spreads has not appeared to worry equity markets still benefitting from accommodative monetary policies although this benefit may be eroded over time as attention turns to the negative growth impact of monetary tightening.

The US dollar retreated in the past week against the currencies of its major trading partners as doubts arose about the progress toward tax reform in the US congress.

The currency would also have been affected by rising doubts about how aggressively the Federal Reserve might pursue interest rate adjustments. The release of the most recent minutes of discussions among policymakers suggested divisions in opinion about how quickly Fed inflation targets would be achieved.

The possibility that inflation remains below target for an unexpectedly prolonged period raises the chances of the Fed's policy approach being reappraised in coming months and shortly after the retirement of Janet Yellen as head of the Federal Reserve.

Commodity prices generally have recovered from the weakest points in the cycle but remain in what could be characterised as a prolonged cyclical tough in which growth in demand has not been sufficient to force prices higher.

Modest gains in daily traded nonferrous metal prices in the past week would have been supported by the weaker US dollar. Prices generally have retreated from the most recent highest prices.

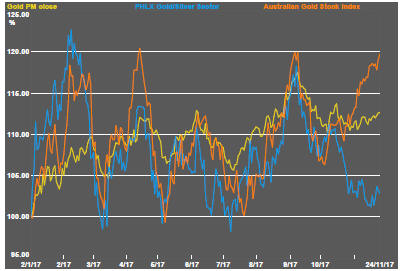

US denominated gold equity prices have appeared less responsive to bullion price movements and are nearing the lower end of the trading range established over the past year.

Within the gold sector, Australian listed gold stocks have performed more strongly than those listed on north American markets, helped by a weaker Australian dollar and some rising bullishness about the discovery potential within Australia.

The Australian gold index is currently at the upper end of the trading range during 2017 even while US prices are trading at the lower end of the range in which they have traded during 2017.

Crude oil prices have reached their highest prices in two years with news that OPEC members and Russia are set to agree to an extended production curtailment agreement.

Uncertainty remains about how US producers will react to higher prices without any incentive for them to curtail output.

The Saudi Arabians, meanwhile, are targeting a 2018 listing of their state owned oil producer which will benefit from the highest possible oil prices when the offer comes to market.

The uranium sector has certainly not recovered but the Cameco announcement that it would cut production at its Cigar Lake project has helped spark some investment interest in the sector.

Despite the market rebalancing which the Cameco announcement implies, the sector remains near the bottom of a prolonged cyclical adjustment.

From an investment perspective, the uranium sector is adding to the evidence that the best returns are from those investments most leveraged to changes in sentiment at the bottom of a cycle. The uranium producers are among the last offering such an opportunity.

The bias for Australian dollar reporting entities is toward more favourable valuations as the Australian dollar trends lower with rising concerns about the longer term growth trajectory of the Australian economy and the limits placed on interest rate adjustments by already flagging house prices.

.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.