The Current View

A lengthy downtrend in sector prices had given way to a relatively stable trajectory after mid 2013 similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability suggests a chance for companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low. These conditions were reversed through 2016 and 2017 although sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

Has Anything Changed?

The strength of the US dollar exchange rate since mid 2014 had added an unusual weight to US dollar prices. Reversal of some of the currency gains has been adding to commodity price strength through 2017.

Signs of cyclical stabilisation in sector equity prices has meant some very strong ‘bottom of the cycle’ gains.

Funding for project development has passed its most difficult phase with the appearance of a stronger risk appetite.

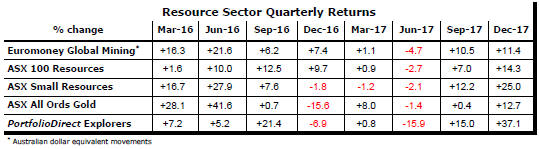

Resource Sector Weekly Returns

Market Breadth Statistics

Market gyrations continued to ease as fears about inflation subsided and investors reconciled themselves to there being an acceptable trade-off between higher interest rates and stronger demand over the coming year.

Uncertainties about policy and the conduct of the US president have replaced some of the macro issues which had contributed to market anxiety.

President Donald Trump has left markets wondering what his tariff policy will look like after he has allowed for exemptions based on ill-defined national security considerations. Threats of retaliation to Trump's tariff policies have raised the profile of trade policy as a detrimental influence on economic conditions just as investors were becoming more confident about the growth outlook.

The continued instability in White House personnel continued to unnerve investors with favourably viewed Gary Cohn deciding to leave his position as the head of economic policy for the administration.

Within the US market, large disparities in performance have persisted including among the more interest rate sensitive sectors where utilities and real estate have greatly underperformed financial services companies.

The information technology grouping remains the market leader.

The latest monthly US labour force statistics (for February) reverted to the long term pattern of strong employment gains with only modest wages increases.

Every month that goes by leads the Federal Reserve to adjust what it believes is full employment (and how that might affect interest rate settings).

The participation rate continues to edge higher even as economists have been describing the US economy as being at or near full employment.

Employment gains are drawing on some two million prime age workers who lost their jobs during the recession but who are yet to return to the workforce. Among this group are many people with African American and Hispanic backgrounds, groups still facing relatively high unemployment rates.

The recent rise in bond yields has remained within the bounds of the decades long downtrend in yields. While downside expectations are limited, the absence of a break above the downtrend will have gone some way to ease tensions about the impact on equity prices of tighter monetary conditions.

A further move higher may not be treated so casually but may be delayed until the full extent of the labour supply pipeline is more clearly evident.

Low grade corporate bond yields have edged up slightly but, taken as a sign of financial conditions for miners, remain consistent with favourable funding conditions which have not deteriorated with the rise in market yilds.

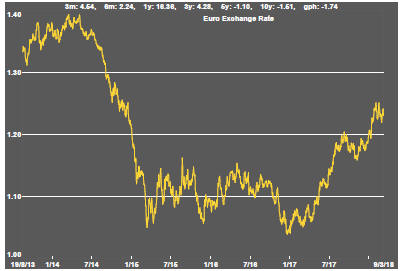

The US dollar has edged higher against the basket of major trading partners' currencies but the directional move has not been strong. The Japanese yen has continued to rise with potentially negative effects on the trade oriented Japanese companies which play such a large role in the Japanese stock market.

The US dollar more generally has lost momentum as a mixture of cross currents, including uncertainties over relative growth rates and how international trade opportunities are likely to evolve, affect outcomes.

Those factors aside, the tug of war between capital flows and interest rate effects will set the direction of the currency once there is greater clarity on those fronts.

If the US was to be producing unambiguously stronger growth outcomes than the rest of the world, dollar appreciation could resume.

If the US is growing sufficiently strongly to support better growth outcomes elsewhere, on the other hand, the dollar could resume its long term decline as capital investment outside the US gains in attractiveness.

An unaddressed government debt problem is likely, at some stage, to reassert its negative influence on the US dollar.

The gentle upward drift in the Australian dollar could remain intact as risks to global economic conditions appear to have been lowered. Within that trend, tightening monetary conditions in the USA and, later, in Europe could exert more downward pressure as they occur.

In the near term, trade disputes between the USA and its major trading partners in Canada, Mexico, Europe, Japan and China could add headwinds for any country potentially caught in the crossfire, including Australia.

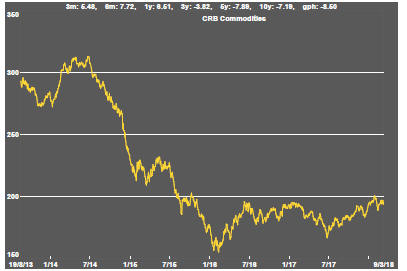

The general upswing in commodity prices remains within the bounds of a cyclical trough suggesting still stronger economic activity will be needed to carry prices higher.

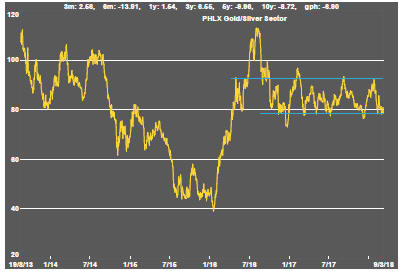

The gold price has been subjected to a tug of war between the negative effect of higher bond yields and the positive influence of a weaker US dollar.

Over the past week, threats to world trade patterns would have added some upward bias to prices which have now moved markedly out of line with the change in bond prices.

The net change in bullion prices has been relatively modest despite the sometimes unusually large swings in macro variables.

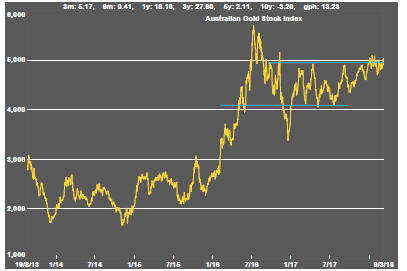

The prices of Australian gold related stocks have moved within a narrower range than their north American counterparts. Australian prices sit around the upper end of the range of outcomes over the past year. In contrast, North American prices are around the lower end of their range.

Both groups of stocks have shown less than historical leverage to higher bullion prices. The North American stocks have shown the stronger connection to weaker equity markets over the past month.

Within the precious metal complex, there has been a 50 percentage point spread in performance with palladium prices racing ahead of relatively stable gold, silver and platinum prices. The rapid upward move in palladium prices has eased.

Prices of the main daily traded nonferrous metals had become increasingly correlated with a broadening consensus about the lowered risks to world economic activity.

Tin prices have lagged conspicuously over the past year but have shown a similar rise to that of other metals since late in 2017.

Prices moved lower last week as concern about disrupted international trade patterns intensified and as (still minor and ambiguous) signs of weakness in Chinese activity rates had an effect.

The bulk commodity response to the change in macro conditions has been stronger within the coal market than for iron ore but both tended negative in the past week.

Demand for iron ore has remained at cyclically high levels but with little change over the past four years in global steel production, the scope for significant tightening in market conditions is more limited than for coal.

The coal market will have been a beneficiary of increasingly constrained supplies with capacity being closed in Asia and development plans elsewhere under threat despite rising demand.

In a similar reaction to that evident among the gold stocks, equity prices for oil and gas explorers have been dominated by broader stock market movements rather than movements in the price of crude oil.

Higher US production remains a burden on investor expectations.

Production cuts appear to have had little sustained effect on sentiment toward uranium investments. This will change eventually but more meaningful cyclical progress still appears many months away.

Investors will be looking to trade equities within a relatively narrow bottom of the cycle trading range.

Eighteen months of rising lithium stock prices has given way to a period of market reassessment as a lengthy pipeline of potential new projects raises the prospect of ongoing supplies being adequate for expected needs.

Potential lithium producers have been able to respond far more quickly to the various market signals than has been the case in other segments of the mining industry.

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.