The Big Picture

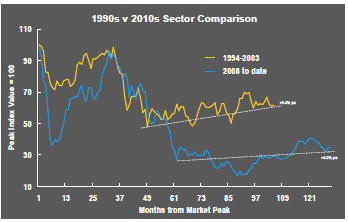

After recovering through 2010, a lengthy downtrend in sector prices between 2011 and 2015 gave way to a relatively stable trajectory similar to that experienced in the latter part of the 1990s and first few years of the 2000s.

The late 1990s and early 2000s was a period of frequent macroeconomic upheaval during which time sector pricing nonetheless proved relatively stable.

Relative stability in sector prices suggests a chance for individual companies genuinely adding value through development success to see their share prices move higher. This was the experience in the late 1990s and early 2000s.

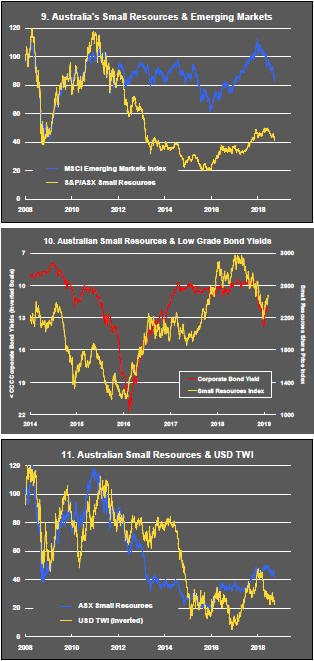

Still vulnerable cyclical conditions were aggravated in the second half of 2015 by a push from investors worldwide to reduce risk. Sector prices were pushed to a new cyclical low some 90 months after the cyclical peak in sector equity prices but these conditions were reversed through 2016 and 2017 although, for the most part, sector prices have done little more than revert to the 2013 levels which had once been regarded as cyclically weak.

With a median decline in prices of ASX-listed resources companies through the cycle of 89%(and 30% of companies suffering a decline of more then 95%), the majority of stocks remain prone to strong 'bottom of the cycle' leverage in response to even slight improvements in conditions.

In the absence of a market force equivalent to the industrialisation of China, which precipitated an upward break in prices in the early 2000s, a moderate upward drift in sector equity prices over the medium term is likely to persist.

The Past Week

The following tables and charts summarise the shorter term influences on investment outcomes for the resources sector.

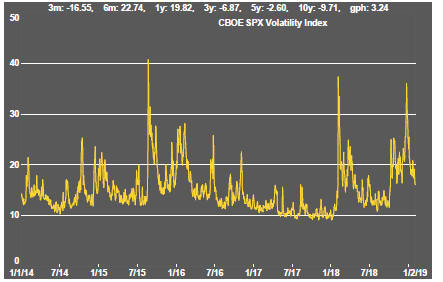

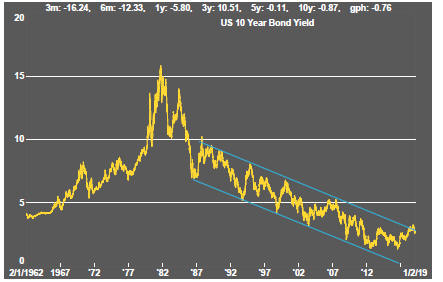

The most important change in the past week has been the evolving stance of the US Federal Reserve about the conduct of monetary policy. Barely a few weeks ago, Fed policymakers were flagging a series of interest rate rises through 2019 and continuing contraction of the Fed's balance sheet. Since the December meeting of policymakers, the stated intent has changed dramatically. Fed chairman Jerome Powell is speaking of patience and waiting to see what the data says before making another move. He has raised the prospect of the balance sheet rundown nearing an end.

The Fed's changed attitude has positive implications for equity prices which have already been seen.

The change in attitude also has important implications for the resources industry outlook. In reducing the risk of interest rates being pushed up too quickly or too far, it potentially delivers a better growth outcome than had otherwise been likely, critical for the cyclical positioning of the industry.

The Fed restatement of policy suggests greater emphasis on market conditions and global economic events than seemed to apply previously. This suggests a more reactive Fed than the one leading a change in policy settings which its moves toward policy normalisation during 2018 had implied.

Strong labour market conditions persisted during January according to the US labour market statistics released on Friday. These data were consistent with the flow of data during 2018 and contrary to movements in equity markets during December. They also run against the view of the Fed that interest rate settings are about right insofar as they suggest that the US economy is continuing to run ahead of its long term potential growth which, prior to the December market slump, was widely seen as necessitating further adjustment.

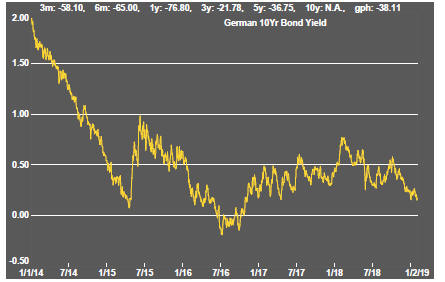

Despite the revised policy stance benefitting growth, the signals from Europe and China in the past week were negative. Consistent with the PortfolioDirect macro view, the global economy is slowing with conditions trending toward more sustainable rates of growth in all major economic regions.

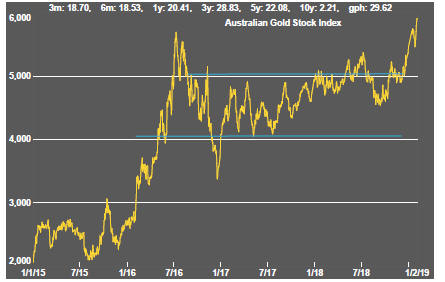

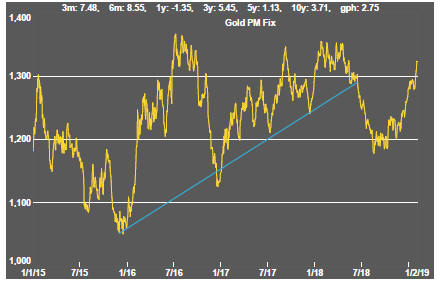

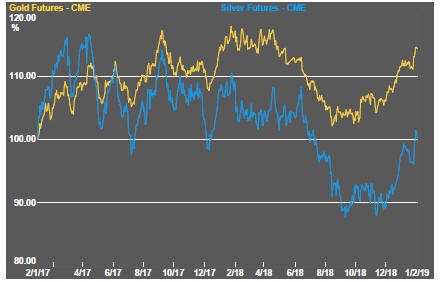

Related to moves in financial markets responding to the revised track of interest rates and the prospects for global economic growth, gold bullion prices have risen with a beneficial impact on gold related equity prices.

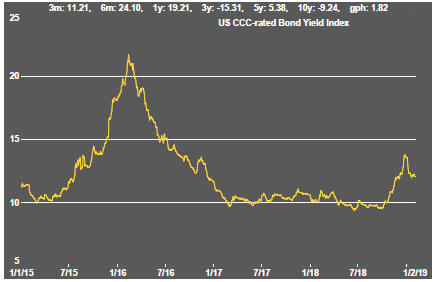

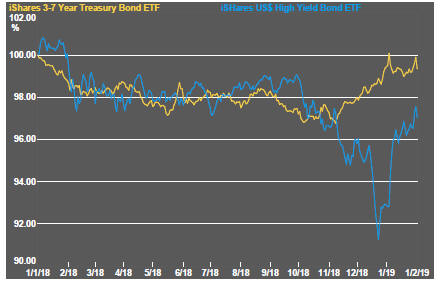

Corporate bond yields for the riskier end of the market have retraced slightly which should support more favorable capital market conditions for early stage miners.

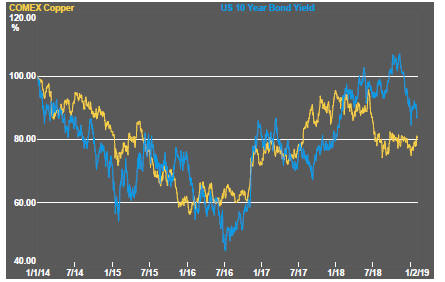

Daily traded nonferrous metal prices have moved above trend compared to the historical cyclical positioning model.

Battery metal related prices have tended to weaken with cobalt continuing on a downtrend and related equity prices underperforming broader sector prices.

Sector Price Outcomes

52 Week Price Ranges

The Steak or Sizzle? blog LINK contains additional commentary on the best performed stocks in the sector and the extent to which their investment outcomes are underpinned by a strong enough value proposition to sustain the gains.

Equity Market Conditions

Resource Sector Equities

Interest Rates

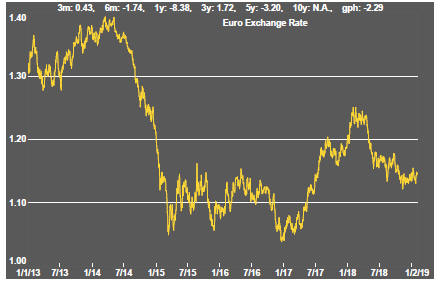

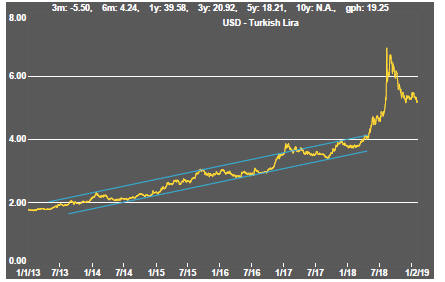

Exchange Rates

Commodity Prices Trends

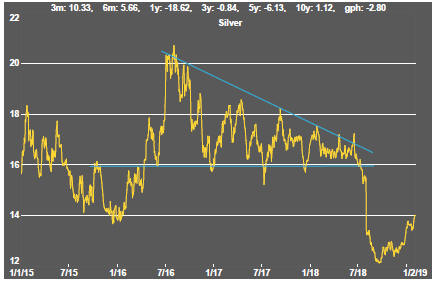

Gold & Precious Metals

Nonferrous Metals

Bulk Commodities

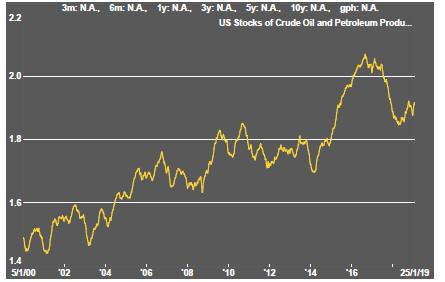

Oil and Gas

Battery Metals

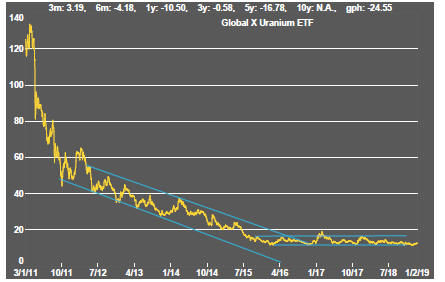

Uranium