-

About

PortfolioDirect -

Subscription

Information

Ironbark Zinc Limited

This summary of views is based on the PortfolioDirect rating criteria described in the detailed PortfolioDirect rating report for Ironbark Zinc Limited dated 6 January 2017. No investment decisions should be taken based on the views presented below. Financial advisers and professional money managers may request a copy of the full Ironbark Zinc rating report from here.

Recent Events

The company has been awarded an Exploitation Licence (Mining Permit) for its Citronen project in Greenland (ASX 19 December 2016).

The company executed an Impact Benefit Agreement with local municipalities (ASX 26 September 2016).

The company raised A$1.5M from a share placement and a further $0.5M from a share purchase plan (1 & 14 April 2016).

Development Stage

PortfolioDirect has classified Ironbark Zinc as a late stage Phase I company. The PortfolioDirect analysis would normally treat a company with a mining permit and a feasibility study as entering Phase II with the rating being a function of the underlying value enhancement arising from the project but, in this instance, the existing feasibility study is several years old making it more akin to a scoping study on which further work must be conducted to offer the requisite degree of confidence about the economics of the project.

Evaluation Summary

Asset Quality

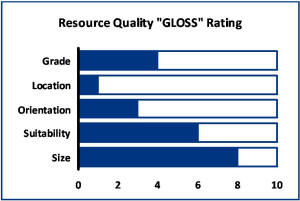

The ‘GLOSS’ rating criteria provide the framework against which the quality of company activities are assessed.

The quality assessment for Ironbark Zinc points to a rating within the lower end of the feasible range of outcomes.

The nature of the mineralisation at Citronen leaves the project with a relatively low

overall ore grade although global mine grades have been falling and

Citronen is nearer the grade of more recently discovered mineral

properties. Discovery of a higher grade component, with the

potential to improve project economics, would depend on the company

undertaking additional exploration activity in the region with

associated delays. In any event, the company may have to complete

additional drilling to raise the confidence attaching to the current

resource estimate as a precursor to a development go-ahead. The

company has not foreshadowed any significant work on this front.

higher grade component, with the

potential to improve project economics, would depend on the company

undertaking additional exploration activity in the region with

associated delays. In any event, the company may have to complete

additional drilling to raise the confidence attaching to the current

resource estimate as a precursor to a development go-ahead. The

company has not foreshadowed any significant work on this front.

The Citronen project is located in one of the most remote and physically hostile locations possible. That does not preclude mining. Arctic mining in north America is well established but requires specialised skills and knowledge which are not commonly available and not readily transferable from base metal mines in Australia.

The geometry of the Citronen mineralisation - distributed in a series of relatively thin, shallowly dipping lenses - will be a constraint on the company’s development plans adding to the complexity of mining operations and development costs.

At the time of the project feasibility study, metallurgical test work had not been finalised. The company has not released definitive data about the metallurgical suitability of the concentrates although the incomplete available data suggest production of material suitable for existing smelters. The absence of significant by-product credits or free metal in the concentrates may affect the attractiveness of the concentrate for some smelters.

At the most recently foreshadowed rate of production, Citronen would be among the 10 largest operating zinc mines. While size is sometimes an indicator of economies of scale, mining scale at Citronen has been dictated in part by the nature of the mineralisation which has negated benefits that might have arisen from a high throughput rate in other circumstances.

Investment Risk Assessment

The risk assessment suggests that Ironbark Zinc is toward the low end of the risk range for a company at its stage of development.

The company’s existing capital is

adequate for only a minimalist approach to development planning

but funding needs will rise with the recent government approval

for mining development.

While the company has frequently cited its connections with larger corporates such as Glencore and Nystar, both have already made financial contributions in exchange for rights to the company’s future production which might have otherwise attracted others with capital to invest.

A more up to date feasibility study may be required before the company can begin assessing the appetite among investors to subscribe for more shares.

At current market prices, the equity funding needed to get development underway will be highly dilutive. In the absence of fresh industry interest or a willingness of existing corporate shareholders to contribute additional equity, a sharply discounted share offering may be necessary to attract a sufficient number of new shareholders.

The company has been promoting the Citronen project for nearly 10 years since purchasing an asset to which a mineral resource had already been attributed suggesting subdued market expectations.

Despite the delays, the company’s investment returns have generally been among the upper one-third of those available to sector investors through the cycle suggesting a relatively resilient set of expectations among investors and a consequential limit on the scope for a value reappraisal in response to the government approval to mine.

The risk of regulatory delay has now been shunted into the background (although actual delays in realising the project have been considerable) by a government keen to take advantage of its mineral endowment to enhance the living standards of its residents.

The risk attaching to finding market openings for the Citronen output is now low. Recent mine closures mean a need for new sources of metal although the extent of that need may have been exaggerated.

The company has also accounted for 70% of its zinc output through off-take arrangements with Glencore and Nystar, minimising the extent to which it is at risk of being unable to sell all of what it can produce.

Opportunity costs for ordinary investors remain potentially challenging. Although the company has received the go-ahead from the Greenland government for mine development to occur, the company is not in a position to commit immediately to project construction. An updated feasibility study which might also require additional drilling to define adequate mineable reserves could push a decision to proceed well into 2017.

Funding this preliminary work as well as the later development requirements will add to the opportunity cost risk as the company is forced to tap shareholders for sufficient funding with possibly highly discounted share offers.

Scope for Future Rating Reappraisal

The PortfolioDirect rating is based on information available

publicly at the time of writing. With greater certainty about

the timing and costs of the Citronen development, Ironbark Zinc

could be reclassified as a Phase II company in which case its

rating will depend more heavily on the underlying valuation that

might be attributable to the Citronen project. Whether this

results in an improved rating will depend on whether the project

can generate a sufficiently strong return on the capital being

invested and whether the project can demonstrate the necessary

positive valuation momentum after taking account of its funding

costs.

Copyright 2016 PortfolioDirect All Rights Reserved.